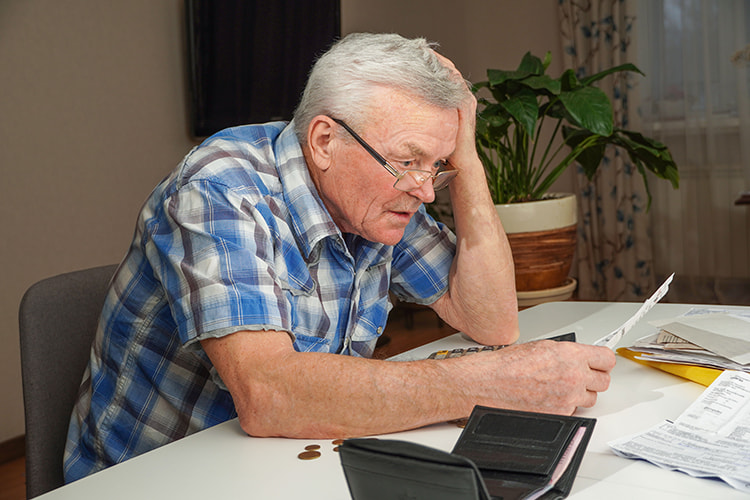

Is your debt keeping you awake at night? Do you struggle to make the minimum monthly payments on your credit cards? Are you worried that you'll never be able to pay back all the debt that you owe?

You might be a candidate for a debt consolidation loan.

When you take out a debt consolidation loan, you combine all or some of your debt into one loan. Then, instead of making several payments to multiple creditors each month, you make one payment every month until you pay your loan.

Debt consolidation loans are the right option for many consumers who are overwhelmed with their debt. However, there are some potential pitfalls to taking out such loans.

Credit Counseling

Before taking out a debt consolidation loan, you should also sign up with a certified credit counselor. A credit counselor can help you create a realistic budget and understand the reasons for your overspending. You do not want to take out a debt consolidation loan only to run up more debt in the future. Unfortunately, many consumers who take out these loans do exactly that.

Be careful to work with an accredited credit counselor. The U.S. Department of Justice maintains a list of approved credit counseling agencies. You can search for agencies that operate in your state.

Debt Consolidation

Once you are ready to take out a debt consolidation loan, interview several providers. Different lenders will offer different interest rates and terms with their loans. You want to shop until you find a debt consolidation loan that provides the fees and interest rates with which you are comfortable.

Remember, the goal is to pay down your debt as quickly as possible. If you take out a debt consolidation loan that comes with an unnecessarily high-interest rate, it will take you longer, and cost you more, to pay down your debt. One of the criticisms of some debt consolidation loans is that consumers can spend more to pay down their debt than they would by just repaying their creditors directly.

Of course, the benefits of a debt consolidation loan are three-fold: First, you'll be making just one payment every month instead of several to a large number of creditors. That simplifies your financial life. Secondly, many debt consolidation providers negotiate with your creditors to lower the amount of money you owe. Finally, when you take out a debt consolidation loan, creditors and collection agencies will no longer harass you. As long you continue to make your monthly payment on time, those intimidating phone calls will stop.

The Downside of Debt Consolidation

Like most ways to reduce your debt, debt consolidation loans do come with some negatives. First, when you take out one of these loans, your three-digit credit score will fall even further. That is a significant problem. Lenders determine who gets loans and at what interest rates based on their credit score. If your credit score is poor, you might struggle to obtain car or mortgage loans. You might even struggle to get approved for a credit card. So when you do you'll be paying higher interest rates for the privilege of borrowing money.

Secondly, you might lose money when taking out a debt consolidation loan. First, you'll be dealing with interest rates that are often high. Secondly, lenders usually charge fees -- they do vary -- to consumers who need debt consolidation loans. This combination means that you might end up paying more money during the long term to pay off your debt with a debt consolidation loan.

Avoiding the Pitfalls

When taking out a debt consolidation loan, make sure to ask the right questions. You want to make sure that your debt consolidation loan is the first step toward a better financial future. You do not wish it to lead you into further financial difficulties.

Ask debt consolidation lenders to provide you a written statement detailing exactly how much your debt consolidation loan will cost. This statement should include your interest rate and any fees associated with the loan. Pay attention to late fees. Make sure they are not exorbitant. You do not want your finances spiraling even further out of control should you make a payment a day or two late.

Next, ask your debt consolidation lender how long it will take you to pay back your debt by making your regular monthly payment. You want to remove your debt as soon as you can. If the length of your debt payback seems too long, it might be time to move to a new debt consolidation lender.

Ask your debt consolidation lender, too, if they will negotiate with your creditors. You want them to try to reduce the amount of money you owe. Many creditors are open to this. They would rather have some of the money that you owe them and figure that by reducing your debt it is more likely that you will pay them back at least part of what you've borrowed.

Never agree to a monthly payment that you are not sure you can afford. You do not want a monthly payment that will represent a financial struggle. Before meeting with a debt consolidation specialist, make sure that you know exactly how much money you can afford to spend each month on paying down your debt.

Finally, do not beat yourself up too much. It is not pleasant to admit that you need help paying back your debts. However, in today's still-challenging economy, you'll be far from alone. Debt consolidation is not a sign of failure. It is a sign that you are willing to take the steps necessary to rebuild your financial health.